Ping An Securities: Looking for "New Era" Emerging Industry Investment Opportunities

"Yunfeng has a fish cup" Hong Kong stocks simulation contest is hot, and the registration transaction is likely to win 600,000 prizes! [Click here to register]

The transformation and upgrading of China's economy has become the trend of the times. Emerging industries are the main direction for the future development of China's economy and the key to a new round of global competition for Chinese companies:

(1) We have stood on the brink of the fourth industrial revolution. It has subversive characteristics such as exponential growth rate and amazing scale effect. The industrialization speed of emerging industries may be much faster than expected.

(2) Real estate as a pillar industry in China will gradually abdicate, and supply-side reform will comprehensively adjust the industries with overcapacity. The core of China's future economic development lies in the "S-curve" of industrial development, that is, replacing the old economy with the new economy and becoming a new kinetic energy for China's economic development.

China's policy support for emerging industries is mainly focused on breaking through technological bottlenecks, providing funding and policy support, accelerating technological transformation of traditional industries, and promoting the development of emerging industrial clusters.

The transformation of emerging industries is imminent:

(1) From the perspective of the development of emerging industries in the world, the speed of emerging industries becoming mainstream may be faster than investors' expectations. Most of the emerging technologies will become mainstream in the next 10 years, bringing disruptive changes to the world economy.

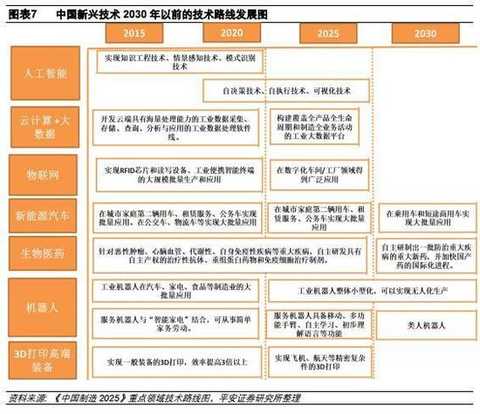

(2) According to the maturity and development space of the emerging industries in the world, we believe that the seven industries of artificial intelligence, cloud computing and big data, Internet of Things, new energy vehicles, biomedicine, robotics and 3D printing are expected to become the new pillars of China's economy. Emerging industries. According to the government's roadmap for emerging technologies, these emerging technologies are expected to be widely used in daily production and life in 2020. In 2025, these emerging industries are expected to achieve further improvements in production efficiency through technological upgrading.

Policy analysis of the seven emerging industries: We analyzed the future development space and speed of the seven major industries and the policy support focus from the three aspects of development goals, existing market size and industrial policies. Most of these industries are in the stage of development, and the future development space is large and the development speed is relatively fast. The government has also recently introduced policies to promote industrial growth by promoting basic technology breakthroughs, cultivating leading enterprises, and promoting industrial applications. With clear industry development trends, strong promotion and support from government policies, and increasing R&D investment of enterprises, China's emerging industries are under good development momentum, and promote Chinese companies to gain more in this round of economic transformation. Strong international competitiveness. ?

A-share emerging industry analysis and investment advice:

(1) Under the conservative estimation that does not consider future explosive growth, the higher valuation of emerging industries now puts higher requirements on the future profit growth rate of the industry. In the short-term, the delay in the expansion of outdated purchases and the tightening of earnings growth in emerging industries may be nearing completion, and the growth rate of emerging industries in the third quarter is expected to bottom out. In the long run, valuations of some emerging industries may be biased. Investors can reduce risks by focusing on “real growthâ€, investment industry leaders and waiting for the industry to mature further.

(2) Recommend investors to pay attention to emerging industry companies with reasonable PEG, obvious layout advantages and strong technical barriers. It is recommended to pay attention to NavInfo, Guanglianda, Dongfang Guoxin, Yitong Century, Yiwei Communication, Penghui Energy, BYD , Founder Motor, Anke Bio, Beida Pharmaceutical, Dongcheng Pharmaceutical, Fosun Pharma, Robot, Eston.

Risk warning: The industrialization process of emerging industries is slower than expected.

1. Emerging industries are the future direction of China's economy

1.1 Standing on the edge of the fourth industrial revolution In the last two years, it seems that a lot of black technology has emerged overnight: AlphaGo defeated the world's first Ke Jie in the world of chess, causing people's concerns about robots replacing humans; FDA approved CAT The launch of the -T therapeutic drug marks the hope that the future of human beings will completely cure cancer in the near future; new energy vehicle technologies and industries are also maturing, and it is expected to completely replace traditional fuel vehicles in the future. The emergence of these black technologies is just a piece of isolation, or does it mark the beginning of a new era? According to the "Fourth Industrial Revolution" written by the founder of the World Davos Economic Forum, Shellus Schwab, we have actually stood on the brink of four industrial revolutions, whether this industrial revolution The scale, breadth, and complexity are completely different from the changes that humans have experienced in the past, and will bring about earth-shaking changes to the entire human society. Humans are always accustomed to thinking about change with linear thinking and using history to speculate on the future. But according to Klaus Schwab, this habit of thinking can greatly underestimate the subversive changes brought about by the fourth industrial revolution. Compared with the previous industrial revolution, the fourth industrial revolution will have the following subversive characteristics:

(1) Speed ​​of exponential development: Due to the popularity of digitalization and information technology, the world has become a highly integrated cloud. Therefore, unlike the previous industrial revolution, this revolution will show an exponential and non-linear development speed.

(2) Amazing scale effect: Digitalization is one of the core of the fourth industrial revolution, and digital means automation, which means that the scale of the company's scale will not decrease or decrease less, the industry's leading enterprises will Will have a larger business scale.

(3) Synergistic effects lead to the emergence of new technologies: Due to the popularity of digitalization, the synergy between different disciplines and findings is also increasing, which will further stimulate the emergence of new technologies, and the emergence of new technologies will be greatly accelerated. From these characteristics of the fourth industrial revolution, we may be able to explain the previous problem, that is, the recent emergence of various black technologies, is not the emergence of isolated phenomena in various disciplines, but precisely the synergy of different disciplines in the fourth industrial revolution, the birth of The new technology continues to produce results. A simple discussion of the characteristics of the fourth industrial revolution may be more abstract, but a direct result of these characteristics of the fourth industrial revolution is that the industrialization speed of emerging industries may enter faster than everyone's expectations. Moreover, the rapid advancement of emerging industries will bring subversive changes to the overall economy and industry. For investors, this means that opportunities and challenges exist at the same time. According to a report released by the Davos World Economic Forum in September 2015, a series of technical tipping points will appear before 2025. These technical tipping points are determined by the World Economic Forum's survey of more than 800 executives and experts from the information and communication technology industry around the world, and are highly authoritative. From this report, we can see that emerging technologies such as Internet of Things, robotics, 3D printing, big data, driverless and artificial intelligence have a greater probability of appearing in our real life before 2025.å¹µ will bring subversive changes to our lives.

1.2 Emerging industries are China's future development direction From the recent establishment of local real estate regulation and control policies, the establishment of a long-term mechanism for real estate regulation and control, and the central bank's “advanced†directional RRR reduction, we can see that the government The determination of real estate regulation and control is very determined. The government's current positioning of the real estate industry is "maintenance", mainly to prevent the sharp decline in real estate investment from harming the Chinese economy, but it is unrealistic to expect the government to "drink the flood" and promote the real estate industry to prosper again. As a pillar industry of China, real estate will gradually abdicate, and emerging industries are the development direction of China's future pillar industries.

In fact, from the time when Premier Li Keqiang mentioned the "S-curve" of industrial development, we can know the overall thinking of the government's current regulation. At the executive meeting of the State Council in February of the 16th and the meeting with Lin Yifu, the president of Peking University’s National Development Institute in May of the 16th, Premier Li Keqiang repeatedly mentioned the “S-curve†theory in industrial economics, which emphasized the growth of old kinetic energy. When it is weak, new industrial kinetic energy has sprung up to support new economic development. Premier Li Keqiang stressed that China's traditional economy has already moved to the ceiling of the S-shaped curve. If it relies on "strong stimulus", it will only cause zombie enterprises, overcapacity, and technological decline. Only by letting the new economy form a new S curve can China be driven. New kinetic energy of the economy. Therefore, for the Chinese economy, whether it is maintaining the real estate market or reducing interest rates, it is a short-term expediency measure. Promoting rapid breakthroughs and industrialization of emerging industries is the long-term strategy for China's economic development. At the time of the reunification, under the impetus of the fourth industrial revolution, the emerging industries may have an exponential rate of development, which has shortened the time for the relay of new and old industries in China.

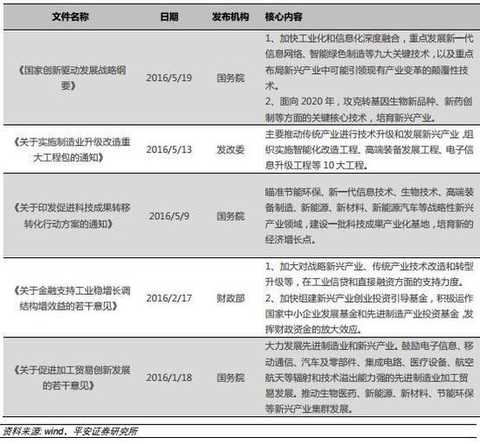

From the perspective of the emerging industrial policies promulgated by the government in the past 16 years, basically the development of the "S-curve" of Premier Li Keqiang has been continued, that is, to promote the rapid development and industrialization of core technologies in emerging industries, while using emerging industry technologies for traditional industries. The upgrading of technology will eventually enable emerging industries to significantly increase their existing productivity and become a new pillar of China's economic development. Specifically, the industrial policies of emerging industries are mainly concentrated in the following four aspects:

1 Break through the technical bottleneck of emerging industries. Deploy a large number of key projects and projects, develop key technologies that break through emerging industries, and proactively deploy disruptive technologies in emerging industries that may cause industrial change.

2 Provide funding and policy support for emerging industries. Accelerate the formation of emerging industry ventures and industrial investment funds, increase capital support for emerging industries, and relax policy restrictions in emerging industries.

3 Accelerate the upgrading of technology in traditional industries. Utilize emerging industry technologies to transform and upgrade traditional industries in terms of intelligence and information, thereby greatly improving the production efficiency of traditional industries.

4 Promote the development of emerging industrial clusters. Accelerate technological R&D and industrial transformation of emerging industries, and form a group of emerging industrial clusters. By 2020, a new generation of information technology, high-end manufacturing, biology, green low-carbon, digital creativity and other five output value scales of 10 trillion yuan will be formed. pillar.

Second, the transformation of emerging industries is imminent

Investors may think that emerging industry technology is still immature, and there is still a long time to go from large-scale popularization, but this may just be an illusion of linear thinking. Some emerging industry technologies are expected to become mainstream in the market within 2-5 years, and will bring earth-shaking changes to the world economy. But at the same time, it is also necessary to be wary that investors have too high expectations for some emerging industries. Once they encounter some problems in industrial application, there may be some risk of retracement. For China, we have identified seven emerging industries that are expected to become the backbone of China's new economy, namely artificial intelligence, cloud computing and big data, Internet of Things, new energy vehicles, biomedicine, robotics and additive manufacturing. According to the government's roadmap for technological development, by 2020, these seven industries will be more widely used in daily life and production.

2.1 The world's emerging industry changes are coming soon

Investors may think that emerging industry technology is still immature, and there is still a long time to go from large-scale popularization, but this may just be an illusion of linear thinking. Some emerging industry technologies are expected to become mainstream in the market within 2-5 years, and will bring earth-shaking changes to the world economy. But at the same time, it is also necessary to be wary that investors have too high expectations for some emerging industries. Once they encounter some problems in industrial application, there may be some risk of retracement. For China, we have identified seven emerging industries that are expected to become the backbone of China's new economy, namely artificial intelligence, cloud computing and big data, Internet of Things, new energy vehicles, biomedicine, robotics and additive manufacturing. According to the government's roadmap for technological development, by 2020, these seven industries will be more widely used in daily life and production.

2.1 The world's emerging industry changes are coming soon

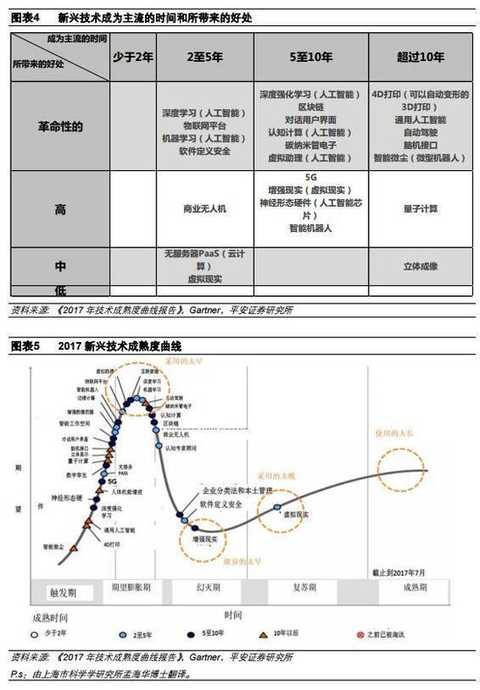

Emerging technologies will become popular in 10 years Although many emerging technologies have emerged, investors may expect that the industrialization of emerging technologies will take a long time due to the immature technology and high cost. But in fact, this may be just a illusion of linear thinking. It is to use the speed of development of the previous industrial revolutions to speculate on the speed of the fourth industrial revolution. According to what we mentioned before, a notable feature of the fourth industrial revolution is the exponential growth rate. Therefore, the popularity and industrialization of emerging technologies may enter faster than investors' expectations.

Gartner is the world's most authoritative IT research and consulting firm. In 2017, Gartner released the “Technology Maturity Curve†report, in which Gartner gave a prediction of the time when the emerging emerging technologies were adopted by the mainstream and the benefits to the economy. Among them, the Internet of Things platform and artificial intelligence are expected to be adopted by the mainstream in 2 to 5 years, bringing about transformative changes to the world economy. In 5-10 years, intelligent robots, VR, 5G and artificial intelligence chips are also expected to be adopted by the mainstream. At the same time, the research and development of artificial intelligence will be further deepened. In 10 years, black technologies such as 4D printing, autonomous driving, micro-robots, and general-purpose artificial intelligence are also expected to become mainstream application technologies, which may bring subversive changes to the world economy. Therefore, although investors intuitively believe that the popularity of emerging technologies may have a long time and there is greater uncertainty, emerging technologies that are rapidly being used by the mainstream may take only 10 years.

Some emerging technologies may be expected to be too high in the short-term. The development speed of the fourth industrial revolution index, the amazing scale effect and the direct synergy of technology have brought greater challenges to investors. On the one hand, due to the subversive development potential of the fourth industrial revolution, investors tend to generate higher expectations. Historically, this often means a technological bubble. On the other hand, because the fourth industrial revolution is different from the characteristics of the previous industrial revolution, even the most insane imagination may underestimate the impact of the fourth industrial revolution. In general, we believe that in the long run, the investment potential of the fourth industrial revolution has not yet been tapped. However, in the short-term, investors may expect too much for some emerging technologies, so that once emerging technologies encounter some setbacks in technology research and development and industrial use, they may cause greater risk of evasion for investors in the short term.

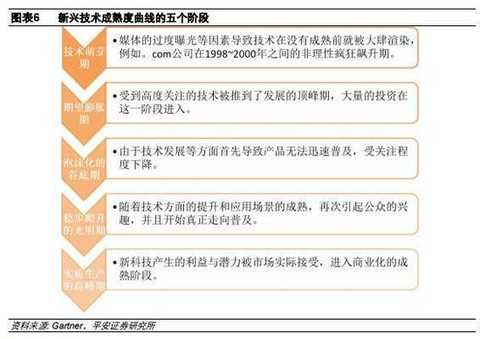

The Gartner technology maturity curve has been released since 1995 and has become an important reference for companies to judge the evolution of new technologies. The vertical axis of Gartner's technology maturity curve is the exposure of the media to the public's expectations for new technologies, while the horizontal axis is the time of technological evolution. The main purpose is to judge whether the new technology is pure media hype or commercial. The Gartner technology maturity curve divides the evolution of emerging technologies into five phases, namely, the germination period of technology, the expected expansion period, the bottom period of foaming, the bright period of steady climb, and the peak period of real production.

On the Gartner technology maturity curve, companies adopting emerging technologies need to avoid four trap periods: 1 adopting new technologies in the early stage of expected expansion, and thus facing the problem of immature technology and high cost, technology bubbles are also often generated. In this period. 2 Abandoning emerging technologies prematurely at the bottom of the bubble. At this time, due to the negative news of technology, the company may give up the adoption of new technology prematurely, but in fact this new technology is about to enter maturity. 3 Use a technique too late in the steadily climbing bright period. At this time, the same type of enterprises on the market have adopted this technology in general, and the late use of new technologies will make enterprises in a disadvantageous position in the competition. 4 The use of technology during the peak period of physical production is too long. At this time, when new technologies are beginning to be phased out, companies need to be prepared for the use of updated technologies.

From the perspective of Gartner's technology maturity curve, emerging technologies such as intelligent robots, the Internet of Things, artificial intelligence, and autonomous driving have entered the expected expansion period. This shows that these technologies have begun to gradually mature, and the media and investors are paying more and more attention to these technologies, and a large amount of investment has begun to enter these fields. It is expected that the expansion period is often the fastest-growing period for emerging technologies, and it is often a period when technology bubbles are easy to generate. It should be noted that the expectation of the expansion period is purely a demonstration of the fact that people's expectations for emerging technologies are too high in the short term, and the speed of future development of technology cannot keep up with people's expectations, but this does not mean that emerging technologies will eventually enter a period of disillusionment. Take consumer 3D printing technology as an example. This technology appeared on the emerging technology maturity curve in 2015, at the end of the expected expansion period, and seems to be entering the disillusionment phase. But this technology disappeared on the emerging technology maturity curve in 2016, meaning that Gartner believes this technology has become the technology of mainstream applications. Therefore, for emerging technologies such as intelligent robots, Internet of Things, artificial intelligence, and autopilot that enter the expected expansion period, we need to realize that investors are paying too much attention to them now, and there is a certain speed of technological development that cannot keep up with the expected risks. But it does not mean that these technologies will enter the bottom of the bubble.

2.2 China's emerging industrial revolution is also coming soon

Gartner's time for emerging technologies to become mainstream technology, as well as the benefits to the economy, we have identified seven emerging industries that are expected to become the new pillars of China's economy, namely artificial intelligence, cloud computing and big data. Internet of Things, new energy vehicles, biomedicine, robotics and additive manufacturing. We believe that these industries are developing at a faster rate and have greater market potential. They are expected to replace traditional industries within the next 10 years and become a new pillar industry of the Chinese economy.

Investors may think that there are certain bottlenecks in the key technologies of these industries, and there are also large uncertainties in the future industrialization. The speed of the pillar industry in the future of China's economy may not be so rapid. However, we believe that investors may still underestimate the speed of rapid development of these industries. In October 2015, the National Manufacturing Powerhouse Construction Strategy Advisory Committee formulated the “Technology Roadmap for China Manufacturing 2025 Key Areasâ€. This technical roadmap mobilized 48 academicians, more than 400 experts and senior management personnel from relevant enterprises to participate. The future development trend of emerging industries has a strong reference value. From this road map, we can see that by 2020, these seven emerging technologies are expected to be widely used in social life and production. By 2025, these seven emerging technologies will not only be popularized in social life and production, but also through technological evolution to further improve production efficiency.

Specifically, by 2020, these emerging industries will see results. For artificial intelligence, Liaobu has developed artificial intelligence software technology, which enables artificial intelligence to achieve a series of functions such as knowledge acquisition and application, situational awareness, pattern recognition, etc. For cloud computing and big data, develop a cloud with storage and processing functions. Industrial data processing software; for the Internet of Things, to achieve large-scale use of RFID chips and reading and writing devices; for new energy vehicles, to achieve small-scale use in the private sector, but in the public service field to achieve large-scale widespread use; for biomedicine It is a key breakthrough in the development of drugs and technologies for the treatment of major diseases by 2025; for robots, the large-scale application of industrial robots in the manufacturing industry can be realized, and the integration of service robots and smart home appliances can be realized; It realizes 3D printing of general equipment and improves the efficiency of manufacturing by more than 3 times.

By 2025, these emerging industries can further improve their production efficiency through technological evolution. For artificial intelligence, it can make decision-making and execution autonomously, and can realize visual perception; for cloud computing and big data, it realizes industrial big data platform covering the whole industry chain production; for the Internet of Things, it is widely used in manufacturing; for new Energy vehicles are used in large quantities in the private sector. For biomedicine, by the year 2030, a number of major new drugs for the prevention and treatment of major diseases have been independently developed. For robots, the overall miniaturization of industrial robots can achieve unmanned production. Service robots are combined with artificial intelligence to achieve humanoid functions; for additive manufacturing, high-end equipment manufacturing precision and complex parts are printed.

Third, the policy analysis of the seven emerging industries

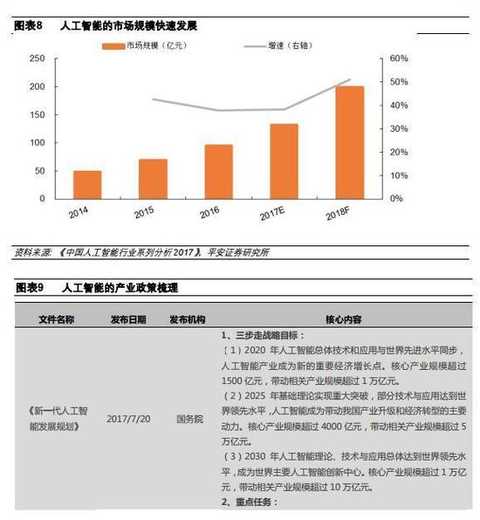

We have previously screened seven industries that are expected to become the new pillars of China's economy in the next 5-10 years, including artificial intelligence, cloud computing and big data, Internet of Things, new energy vehicles, biomedicine, industrial robots and additive manufacturing. The Chinese government also attaches great importance to these seven emerging industries and has issued a large number of policy documents to support the development of these industries. We separately analyzed the future development space and development speed of the seven major industries, as well as the policy support focus from the three aspects of development goals, existing market size and industrial policy. Investors can focus on the investment opportunities brought about by these support policies. 3.1 Artificial Intelligence From the perspective of future development goals, the government attaches great importance to the development of artificial intelligence and cultivates artificial intelligence as a pillar industry in the future. According to the "New Generation Artificial Intelligence Development Plan", the government plans to synchronize the overall technology and application of artificial intelligence with the world's advanced level in 2020. The core industry scale exceeds 150 billion yuan, and the scale of related industries exceeds one trillion. In 2025, artificial intelligence was used as the main driving force for China's industrial upgrading and economic transformation. The core industry scale exceeded 400 billion yuan, and the scale of related industries exceeded 5 trillion yuan.

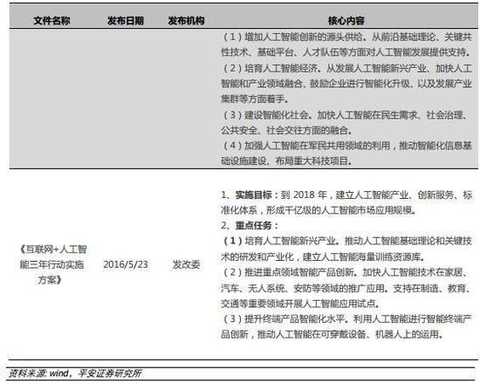

From the perspective of the existing industry scale, China's artificial intelligence industry is still in its infancy, and there is still much room for development in the future. In 2016, the market scale of artificial intelligence was only 9.661 billion yuan, and there is still much room for development from the government planning target of 2020 billion in 2020. In addition, the market scale of artificial intelligence has also maintained a relatively high growth rate. The year-on-year growth rates in 15 and 16 years were 42.69% and 37.93%, respectively. Moreover, the growth rate of artificial intelligence market has been increasing. It is expected that by 2020, the artificial intelligence market will maintain a high average annual growth rate. From the perspective of industrial policies, the government's industrial support for artificial intelligence mainly focuses on three aspects: developing basic technologies, accelerating industrial integration, and building an intelligent society:

1 Develop the technical basis of artificial intelligence. Including the development of cutting-edge basic theory, the establishment of artificial intelligence massive training resource library.

2 cultivate artificial intelligence industry. Mainly to accelerate the integration of artificial intelligence and industry, and encourage enterprises to carry out intelligent upgrades. Through artificial intelligence to greatly increase the production capacity of enterprises.

3 Building an intelligent society. It mainly includes two aspects. One is to promote the innovation of intelligent products and accelerate the application of artificial intelligence in the fields of home, automobile, unmanned system and security. The matter is to accelerate the application and integration of artificial intelligence in the field of social public services, including social governance and public safety.

3.2 Cloud Computing and Big Data

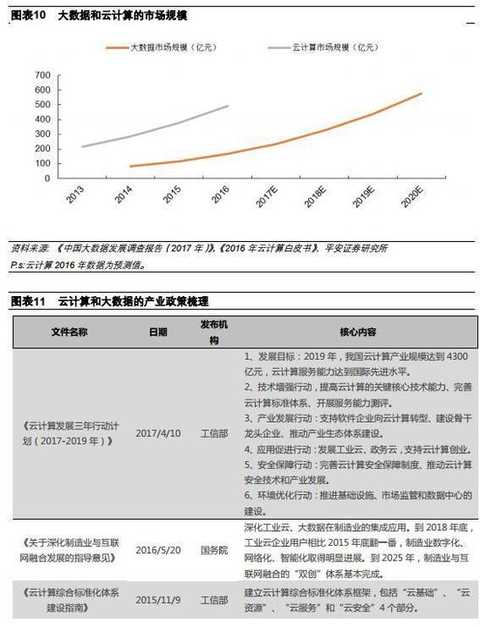

From the perspective of future development goals, the government plans to make China's cloud computing industry reach 430 billion yuan in 2019; it plans to make China's big data products and services revenue exceed 1 trillion yuan in 2020, with an average annual compound growth rate. More than 30%. From the perspective of the existing market scale, China's cloud computing and big data market is still developing in a flood season, and the growth rate is relatively fast. The market size of cloud computing and big data in 2015 was only 37.8 billion yuan and 11.6 billion yuan. There is still much room for development from the government-planned cloud computing market and the big data market. In addition, the scale of cloud computing and big data market has maintained a high growth rate. The market growth rate since 2015 has remained above 30%. The future of such rapid development is also expected to continue. From the perspective of industrial policies, the government's industrial policies for cloud computing and big data are mainly concentrated in four aspects: basic technology, industrial entities, industry applications and security:

1 Develop basic technology. It mainly includes the promotion of cloud computing and big data development in key technologies and standards systems, and the establishment of a national laboratory for big data basic technology and application technology.

2 cultivate the main body of the industry. It mainly includes supporting software companies to transform into computing and big data, and fostering a large number of leading and backbone enterprises.

3 Promote industry applications. It mainly includes the promotion of cloud computing and big data in industrial, agricultural, medical and public services.

4 Establish a security system. It is mainly to improve the development of cloud computing and big data security systems, and promote the development of security technologies and industries in related industries.

3.3 Internet of Things From the perspective of future development goals, the government's industrial policy mainly emphasizes the application of the Internet of Things in various industries, and does not set a general development goal. The application industry of the Internet of Things mainly includes car networking, smart transportation and agricultural cloud networking. For the Internet of Vehicles, the government plans to reach international synchronization level by 2020, and enter the world's advanced forefront in 2025. For smart transportation, the government plans to achieve “one network joint control†for key vehicles (ships) in 2018. For the agricultural Internet of Things, the government plans to use 17% of the agricultural cloud network by 2020. From the perspective of the existing market scale, the industrial chain and industrial system of our Internet of Things have been formed step by step. In 2015, the market scale reached 750 billion yuan. From the perspective of scale growth, with the continuous development of the cloud networking market, the scale growth rate has also declined. However, until 2020, the growth rate of China's Internet of Things is expected to remain above 15%. It is expected that the market size in 2020 may reach 1.83 trillion, which is 2.44 times the size of the 750 billion market in 2015. From the perspective of industrial policies, the government's industrial policy for the Internet of Things is mainly focused on infrastructure construction, as well as vehicle networking, smart transportation and agricultural Internet of Things construction:

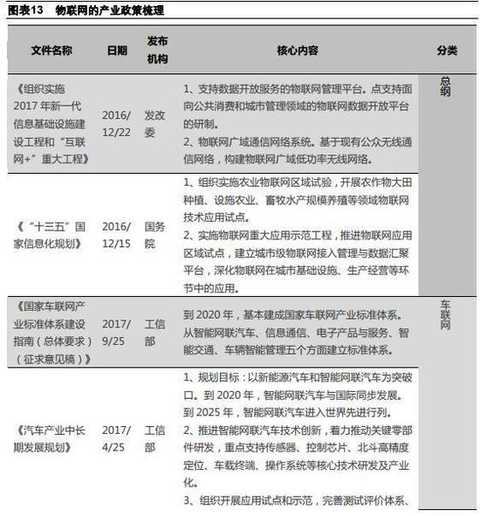

1 Promote the construction of the Internet of Things infrastructure. It mainly includes the construction of the Internet of Things management platform and the Internet of Things communication network system, as well as the implementation of the IoT major application demonstration project, and the promotion of the IoT application area pilot.

2 Promote the construction of the Internet of Vehicles. This includes establishing a vehicle networking standard system, promoting the development of key components, and establishing application pilots.

3 Promote the construction of smart transportation. This includes building a ubiquitous transportation Internet of Things and accelerating the construction of IoT for public vehicles and ships.

4 Promote the construction of agricultural Internet of Things. Including the transformation of the Internet of Things in field planting, livestock and poultry breeding, fishery production, etc., and the establishment of agricultural cloud networking application pilots.

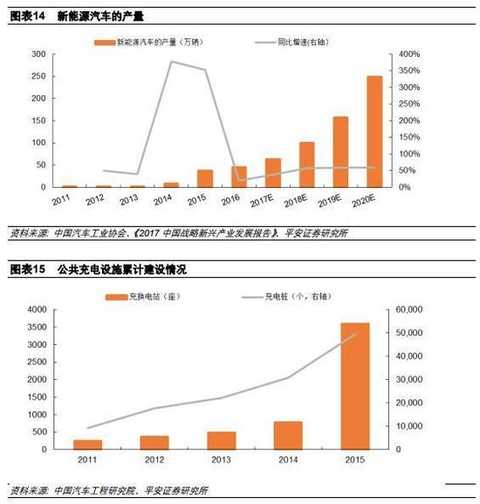

3.4 New energy vehicles From the perspective of future development goals, the government plans to achieve 2 million new annual production and sales of new energy vehicles by 2020, more than 12,000 new centralized charging and replacement stations, and more than 4.8 million distributed charging piles. Cultivate a number of new energy auto companies that have entered the top ten in the world. By 2025, new energy vehicles account for more than 20% of total automobile production and sales.

Judging from the existing market scale, our new energy vehicle production and public charging facilities are still in the development stage, and the future development potential is large. From the perspective of new energy vehicle production, the output of China's new energy vehicles in 2016 was 455,000 units, which is still far from the government's production target of 2 million units in 2020. It is expected that the output of China's new energy vehicles will continue to maintain rapid growth in the future, and the average annual production growth rate in 17~20 years may be above 50%. From the perspective of public charging facilities, the construction of public charging facilities in China is still in its infancy.

In 2015, a total of 3,600 charging and replacing stations and 49,000 charging piles were built. According to the government's goal of adding 12,000 new power stations and charging stations with more than 4.8 million charging piles in 2020, the future development potential of public charging facilities is huge. From the perspective of industrial policy, the government's industrial support for new energy vehicles is mainly concentrated on the use of new energy vehicles, charging facilities and lithium battery research and development:

1 Expand the use of new energy vehicles. Gradually increase the proportion of new energy vehicles used in the public service sector and expand the scale of new energy vehicle applications in the private sector. Encourage the development and use of new energy vehicles in key areas of air pollution control such as Beijing-Tianjin-Hebei.

2 speed up the construction of charging facilities. Strengthen the renovation of charging facilities in existing residential areas, promote the construction of charging infrastructure in public service areas, user residences, and internal parking lots of the units, and build a convenient and efficient charging network system.

3 Increase the research and development of lithium batteries. The construction of the power battery innovation center and the implementation of the power battery upgrading project will achieve large-scale application by 2020.

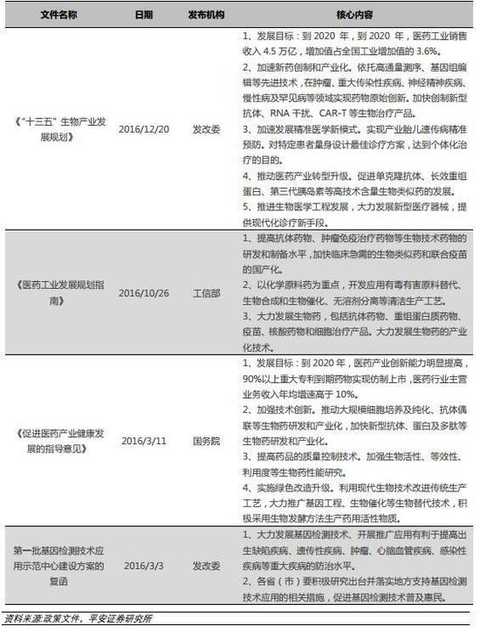

3.5 Biomedicine

From the perspective of future development goals, the government plans to achieve a sales volume of 4.5 trillion yuan in the pharmaceutical industry in 2020, and build 10-20 biomedical professional parks with an output value of over 10 billion.

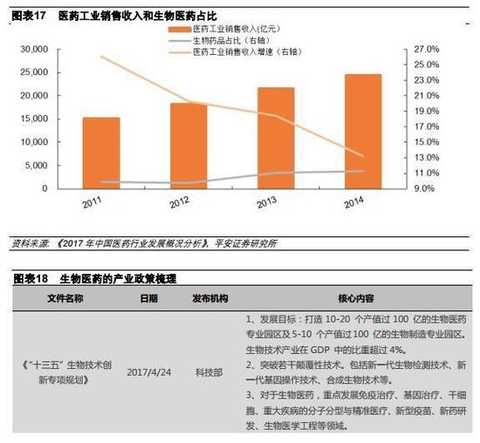

Strategy and strategy, please be sure to read the text after the exemption clause 21 / 31 From the perspective of the existing market size, China's pharmaceutical industry sales revenue in 2014 was 2.4 trillion, according to government plans, by 2020, China's pharmaceutical sales revenue is expected in 2014 The basis is almost doubled. From 2014 to 2020, the average annual growth rate of China's pharmaceutical industry sales revenue may remain at around 11%. In 2014, China's biopharmaceutical sales revenue was 274.7 billion yuan, accounting for 11.26% of all pharmaceutical industry sales revenue. The proportion is still low, and there is room for improvement in the future. In the future, with the increase in the proportion of sales of biopharmaceuticals, the average annual growth rate of biopharmaceuticals from 2014 to 2020 is expected to be higher than the average annual growth rate of 11% of pharmaceutical industry sales. From the perspective of industrial policies, the government's industrial policy support for biomedicine basically focuses on three aspects: bio-new drug development, biosimilar drug development, and precision medicine:

1 biological new drug development. It mainly includes two aspects. First, the use of biotechnology to achieve new drug development in the fields of cancer, major infectious diseases, neuropsychiatric diseases, chronic diseases and rare diseases. The matter is to speed up research and development in the development of new antibodies, RNA interference, CAR-T and other biological treatment products.

2 Biosimilar drug development. Promote the development of high-tech biosimilar drugs such as monoclonal antibodies, long-acting recombinant proteins, and third-generation insulin.

3 develop precision medicine. Using genetic testing technology to achieve accurate prevention of fetal genetic diseases. At the same time, it is also possible to design the best diagnosis and treatment plan for a specific patient to achieve the purpose of individualized treatment.

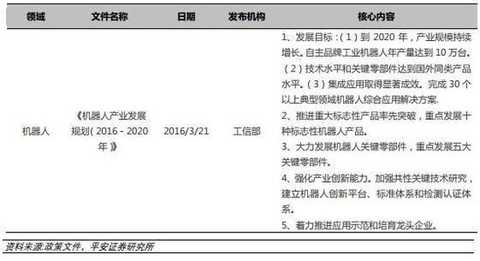

3.6 Industrial Machines

From the perspective of future development goals, the government plans to achieve an annual production of 100,000 independent industrial robots by 2020. The technical level and key components will reach the level of similar foreign products. The integrated application of industrial robots has achieved remarkable results, completing more than 30 typical field robot integrated application solutions. From the perspective of the existing market scale, the sales volume of industrial robots in China has reached 67,000 units in 2015, and the average annual growth rate has reached 59% from 2010 to 2015. In this respect, the demand for industrial robots in China is relatively large. ,Market has great potential. However, in the strategy and strategy topic, please be sure to read the text after the exemption clause 23/31 in the 67,000 industrial robot sales, the domestic market share of domestic robots is only 31%, that is, only 21,000 units. The sales volume of domestic robots in 2015 is still quite different from the sales of 100,000 units planned by the 2020 government. If we want to meet the government-sponsored 2010 domestic robot sales target, then from 2016 to 2020, the annual growth rate of domestic robot sales will be above 36%.

Therefore, domestic robots still have great development potential in the next five years. From the perspective of industrial policies, the government's support policies for independent quality robots mainly focus on establishing standard systems, developing key products and key components, and promoting industrial applications:

1 Establish a standard system. It is mainly to establish the selection and testing standards of robots and robot demonstration enterprises, which helps to improve the overall quality of domestic industrial robots and prevent the shoddy robots from “bad money to drive out good moneyâ€.

2 Promote the research and development of key products and key components. It mainly includes 10 kinds of robotic iconic products such as arc welding robot and fully autonomous programming intelligent industrial robot, as well as five key components such as reducer, motor and driver.

3 Promote industrial applications. The main purpose is to promote the industrial application of industrial robots by establishing robot applications and pilot demonstrations, and establishing robot innovation platforms.

3.7 Additive Manufacturing (3D Printing)

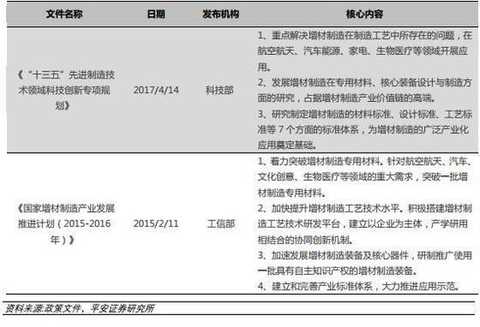

From the perspective of future development goals, the government's planning is more focused on basic theoretical research, mainly focusing on solving various problems in additive manufacturing processes, equipment and special materials, which indicates that the country may not fully grasp the problems. The technology of industrialized additive manufacturing, the existing industrialization of domestic additive manufacturing is still at a relatively early stage, and the industrialization of domestic additive manufacturing may rely more on imported equipment and materials. From the perspective of the existing market scale, although China may not fully grasp the technology of industrialized additive manufacturing, the domestic demand for additive manufacturing is still quite strong. The total of domestic additive manufacturing in 2016 and the first half of 2017 The output value was 2.03 billion yuan and 1.16 billion yuan respectively, with a year-on-year growth rate of 87.50% and 50.50%, respectively, showing an explosive growth.从世界范围æ¥çœ‹ï¼Œå…¨çƒå¢žæåˆ¶é€ äº§ä¸šä¸€ç›´ä¿æŒç€é«˜é€Ÿå¢žé•¿çš„å±€é¢ï¼Œ2016å¹´å…¨çƒå¢žæåˆ¶é€ äº§ä¸šå·²ç»è¾¾åˆ°äº†60.6亿美元,2011~2016å¹´çš„å¹´å‡å¢žé€Ÿçº¦ä¸º30%。而美国的Stratasysã€3DSystemsã€EOSç‰å¢žæåˆ¶é€ çš„é¾™å¤´å…¬å¸éƒ½å·²ç»æˆåŠŸçš„实施了产业化è¿ä½œï¼Œæˆä¸ºä¸–界增æåˆ¶é€ äº§ä¸šåŒ–çš„è¿ä½œæ¥·æ¨¡ã€‚å› æ¤ï¼Œå¢žæåˆ¶é€ çš„äº§ä¸šåŒ–æ˜¯å¯è¡Œçš„,并且有了美国的ç»éªŒä½œä¸ºå‚考,ä¸å›½çš„增æåˆ¶é€ äº§ä¸šåœ¨æœªæ¥10年也有望迎æ¥é«˜é€Ÿå‘展期。从产业政ç–æ¥çœ‹ï¼Œæ”¿åºœçš„扶æŒæ”¿ç–主è¦é›†ä¸åœ¨åˆ¶é€ 工艺ã€æ ‡å‡†ä½“系建立以åŠè¡Œä¸šåº”用三方é¢ï¼š

①完善增æåˆ¶é€ çš„åˆ¶é€ å·¥è‰ºã€‚é‡ç‚¹è§£å†³å¢žæåˆ¶é€ åœ¨åˆ¶é€ å·¥è‰ºã€è£…å¤‡åˆ¶é€ å’Œä¸“ç”¨æ料所å˜åœ¨çš„问题,å æ®å¢žæåˆ¶é€ äº§ä¸šä»·å€¼é“¾çš„é«˜ç«¯ã€‚

â‘¡å»ºç«‹æ ‡å‡†ä½“ç³»ã€‚ç ”ç©¶åˆ¶å®šå¢žæåˆ¶é€ åœ¨ææ–™æ ‡å‡†ã€è®¾è®¡æ ‡å‡†ã€å·¥è‰ºæ ‡å‡†ç‰7个方é¢çš„æ ‡å‡†ä½“ç³»ï¼Œä¸ºå¢žæåˆ¶é€ çš„å¹¿æ³›äº§ä¸šåŒ–åº”ç”¨å¥ å®šåŸºç¡€ã€‚

③推动增æåˆ¶é€ è¡Œä¸šåº”ç”¨ã€‚é’ˆå¯¹èˆªç©ºèˆªå¤©ã€æ±½è½¦ã€æ–‡åŒ–创æ„ã€ç”Ÿç‰©åŒ»ç–—ç‰é¢†åŸŸï¼Œé‡ç‚¹ç ”åŽä¸€æ‰¹å¢žæåˆ¶é€ ä¸“ç”¨æ料,并在这些领域展开应用。

å››ã€A股新兴产业分æžåŠæŠ•èµ„建议

4.1çŸæœŸä¸šç»©è§¦åº•å弹,长期估值略微å高我们认为在第四次工业é©å‘½çš„大背景ã€ä»¥åŠå›½å®¶æ”¿ç–大力推动下,七大新兴产业æˆä¸ºä¸å›½æœªæ¥ç»æµŽæ–°æ”¯æŸ±çš„å‘展速度以åŠæœ€ç»ˆçš„市场空间有å¯èƒ½ä¼šè¶…过投资者的预期。但是在ä¸è€ƒè™‘爆å‘å¼å¢žé•¿çš„ä¿å®ˆä¼°è®¡ä¸‹ï¼Œæ–°å…´äº§ä¸šçŽ°åœ¨è¾ƒé«˜çš„估值对于未æ¥çš„盈利增速æ出了较高的è¦æ±‚,一旦盈利增速ä¸è¾¾é¢„期,则股价å¯èƒ½ä¼šå‡ºçŽ°è¾ƒå¤§çš„回撤。从å¯èƒ½å¯¼è‡´ç›ˆåˆ©å¢žé€Ÿå¤§å¹…ä¸‹æ»‘çš„é£Žé™©å› ç´ æ¥çœ‹ï¼ŒçŸæœŸä¸»è¦æ˜¯å¤–延并è´å®šå¢žç›‘管趋严,而长期则是行业内生æˆé•¿æ€§ä¸è¾¾é¢„期。我们认为,çŸæœŸå¤–延并è´å®šå¢žè¶‹ä¸¥å¯¹æ–°å…´è¡Œä¸šç›ˆåˆ©å¢žé€Ÿçš„æ‹–ç´¯å¯èƒ½å·²ç»æŽ¥è¿‘尾声,三å£åº¦æ–°å…´è¡Œä¸šçš„业绩增速有望触底回å‡ã€‚而长期æ¥çœ‹ï¼Œåœ¨æœªå‡ºçŽ°çˆ†å‘å¼å¢žé•¿çš„情况下,部分新兴行业的估值å¯èƒ½æœ‰æ‰€å高,投资者å¯ä»¥é€šè¿‡èšç„¦â€œçœŸæˆé•¿â€ã€æŠ•èµ„行业龙头以åŠé™å¾…产业进一æ¥æˆç†Ÿçš„æ–¹å¼æ¥é™ä½Žé£Žé™©ã€‚

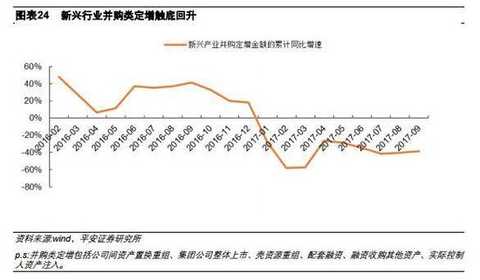

çŸæœŸæ–°å…´è¡Œä¸šä¸šç»©æœ‰æœ›åå¼¹éšç€å¹¶è´é‡ç»„趋严以åŠå†èžèµ„监管趋严,A股并è´ç±»å®šå¢žé‡‘é¢åœ¨17å¹´æœ‰è¾ƒå¤§å¹…åº¦çš„ä¸‹è·Œï¼Œå› æ¤éƒ¨åˆ†æŠ•èµ„者开始担心外延并è´çš„大幅å‡å°‘å¯èƒ½ä¼šå¯¹æ–°å…´äº§ä¸šçš„盈利增速产生较大幅度的负é¢å½±å“。从新兴产业并è´ç±»å®šå¢žé‡‘é¢çš„累计åŒæ¯”增速æ¥çœ‹ï¼Œæ–°å…´äº§ä¸šçš„并è´ç±»å®šå¢žåœ¨17Q1有较大幅度的下跌,但是éšåŽå¼€å§‹å弹,在17Q2åŽåŸºæœ¬ä¸Šç¨³å®šåœ¨-40%å·¦å³ã€‚而部分新兴行业在17Q2的盈利增速相比去年åŒæœŸæœ‰è¾ƒå¤§å¹…åº¦çš„ä¸‹è·Œï¼Œå› æ¤ï¼Œæˆ‘们认为外延并è´å‡å°‘对于新兴产业盈利增速的负é¢ä½œç”¨å¯èƒ½å·²ç»ä½“现在新兴产业事å£åº¦çš„盈利增速上了。

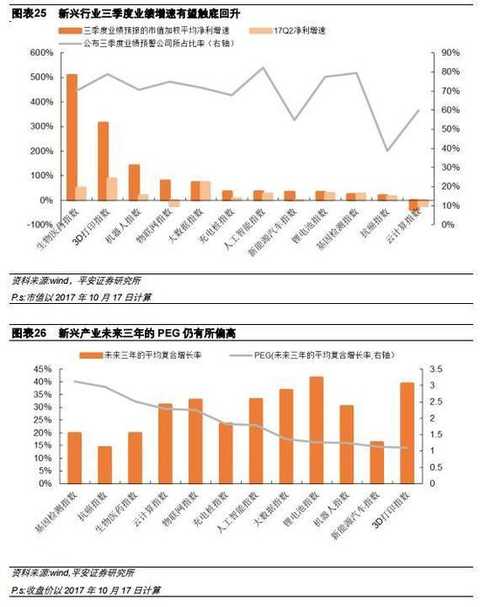

而从新兴产业上市公å¸çš„17Q3的业绩预报上æ¥çœ‹ï¼Œå¤§éƒ¨åˆ†æ–°å…´äº§ä¸šæŒ‡æ•°70%以上的上市公å¸éƒ½å…¬å¸ƒäº†ä¸šç»©é¢„æŠ¥ï¼Œå› æ¤å…·æœ‰è¾ƒå¼ºçš„代表性。我们å–å„个上市公å¸çš„盈利增速预报平å‡å€¼è¿›è¡Œå¸‚å€¼åŠ æƒè®¡ç®—,我们å‘现大部分新兴产业17Q3盈利增速预报è¦å¥½äºŽ17Q2的盈利增速,åªæœ‰åŸºå› 检测ã€äº‘计算17Q3盈利增速预报è¦å·®äºŽ17Q2ã€‚å› æ¤ï¼Œæˆ‘们认为新增外延并è´å®šå¢žå‡å°‘对于新兴产业çŸæœŸç›ˆåˆ©å¢žé€Ÿçš„è´Ÿé¢å½±å“å¯èƒ½å·²ç»æŽ¥è¿‘尾声,在新兴产业已有外延并è´æ ‡çš„业绩ä¸å‡ºçŽ°å¤§å¹…ä¸è¾¾æ‰¿è¯ºçš„情况下,新兴产业çŸæœŸç›ˆåˆ©å¢žé€Ÿç»§ç»å‡ºçŽ°è¾ƒå¤§å¹…度下跌的概率较å°ã€‚

长期新兴产业的估值略微å高总的æ¥è¯´ï¼Œå¦‚果以较长的投资周期æ¥çœ‹ï¼Œæˆ‘们认为新兴产业的现在整体估值å¯èƒ½è¿˜æ˜¯ç•¥å¾®å高,所有的新兴产业的PEG都在1以上,部分行业的PEG更是达到3以上。新兴产业过高的PEGä¸ä¸€å®šæ„味ç€è‚¡ç¥¨ä¼°å€¼è¿‡é«˜ï¼Œæœ‰ä»¥ä¸‹åŽŸå› å¯ä»¥è§£é‡Šä¼°å€¼çš„åˆç†æ€§ï¼š

â‘ ç ”å‘周期过长导致业绩还未释放。在新兴产业ä¸ï¼Œå¯ä»¥å‘现和医è¯ç›¸å…³çš„åŸºå› æ£€æµ‹ã€æŠ—癌和生物医è¯çš„PEGè¾ƒé«˜ï¼Œè¿™äº›è¡Œä¸šçš„ç ”å‘周期较长,产业还未进入高速æˆé•¿æœŸï¼Œæ‰€ä»¥çŸæœŸçš„PEGå¯èƒ½è¾ƒé«˜ã€‚

②第四次工业é©å‘½çš„指数级å‘展速度和规模效应。在对新兴行业未æ¥ä¸‰å¹´ç›ˆåˆ©å¢žé€Ÿè¿›è¡Œé¢„测时,å‡è®¾äº†ç›ˆåˆ©å¢žé€Ÿæ˜¯é€å¹´é€’å‡çš„ã€‚ä½†æ˜¯æ ¹æ®ç¬¬å››æ¬¡å·¥ä¸šé©å‘½çš„特性,新兴产业的å‘展速度å¯èƒ½æ˜¯ä¸æ–递增,并ä¸æ–å‘龙头èšé›†çš„ã€‚å› æ¤ï¼Œæ–°å…´è¡Œä¸šçš„盈利增速预测å¯èƒ½ä½Žä¼°äº†è¡Œä¸šï¼Œå°¤å…¶æ˜¯è¡Œä¸šé¾™å¤´æœªæ¥çš„盈利增速,从而高估了PEG。

但是å³ä½¿æœ‰ä»¥ä¸Šçš„åŽŸå› ï¼Œå‡ºäºŽæ高安全边际的考虑,我们建议投资者å¯ä»¥é‡‡å–以下的方å¼æ¥é™ä½Žæ–°å…´äº§ä¸šçš„投资风险:

①选择具有真实业绩的“真æˆé•¿â€å…¬å¸ã€‚选择新兴产业业务收入å 比较大,且具有一定技术å£åž’的“真æˆé•¿â€å…¬å¸ï¼Œè€Œä¸é€‰æ‹©ç‚’作转型概念的“伪æˆé•¿â€å…¬å¸ï¼Œâ€œçœŸæˆé•¿â€å’Œâ€œä¼ªæˆé•¿â€çš„分化å¯èƒ½ä¼šå¤§å¹…åŠ å‰§ã€‚

â‘¡æŒæœ‰æ–°å…´äº§ä¸šè¡Œä¸šé¾™å¤´ã€‚由于第四次工业é©å‘½å…·æœ‰è¾ƒé«˜çš„规模化效应,行业龙头未æ¥å¯èƒ½å…·æœ‰æ›´é«˜çš„盈利增速。

â‘¢å¯ä»¥é™ç‰æ–°å…´äº§ä¸šåŒ–进一æ¥æˆç†Ÿçš„时候进入,这时候行业的盈利增速会有所下é™ï¼Œä½†PEGå¯èƒ½ä¸‹é™çš„幅度更大,从而带æ¥æ›´é«˜çš„安全边际。

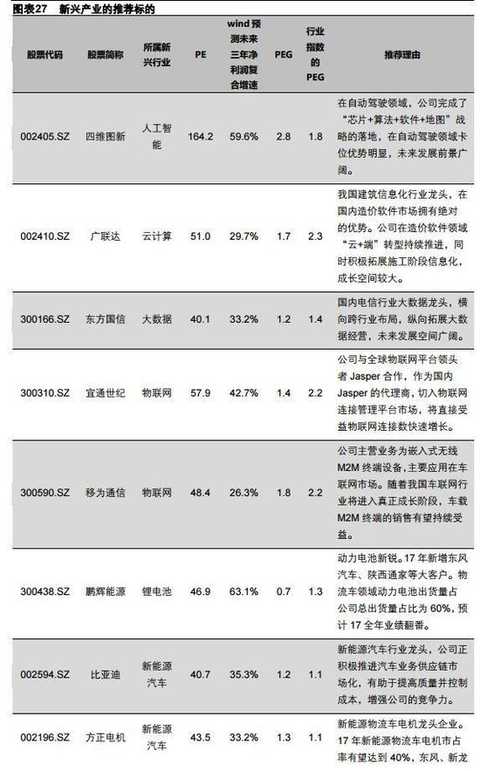

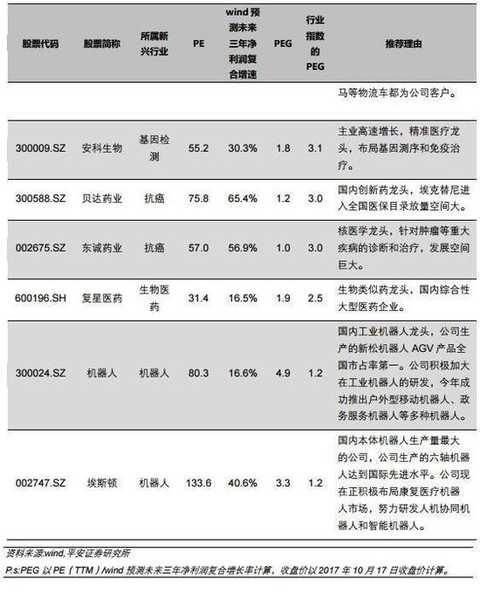

4.2 æŠ•èµ„æ ‡çš„æŽ¨è对于新兴产业的推èæ ‡çš„ï¼Œæˆ‘ä»¬æŽ¨è投资者关注PEG 相对åˆç†ã€åœ¨æ–°å…´äº§ä¸šå¸ƒå±€ä¼˜åŠ¿æ˜Žæ˜¾ã€å…·æœ‰è¾ƒå¼ºæŠ€æœ¯å£åž’的上市公å¸ï¼ŒæŽ¨è投资者é‡ç‚¹å…³æ³¨å››ç»´å›¾æ–°ã€å¹¿è”è¾¾ã€ä¸œæ–¹å›½ä¿¡ã€å®œé€šä¸–纪ã€ç§»ä¸ºé€šä¿¡ã€é¹è¾‰èƒ½æºã€æ¯”亚迪ã€æ–¹æ£ç”µæœºã€å®‰ç§‘生物ã€è´è¾¾è¯ä¸šã€ä¸œè¯šè¯ä¸šã€å¤æ˜ŸåŒ»è¯ã€æœºå™¨äººã€åŸƒæ–¯é¡¿ã€‚

五〠风险æ示

æ–°å…´äº§ä¸šåœ¨æŠ€æœ¯ç ”å‘或产业化过程ä¸ï¼ŒçŸæœŸé‡åˆ°ä¸€å®šçš„瓶颈,从而导致新兴产业产业化进程慢于预期。

Sina statement: This news is reproduced from the Sina cooperation media, Sina.com posted this article for the purpose of transmitting more information, does not mean agree with its views or confirm its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.

进入ã€æ–°æµªè´¢ç»è‚¡å§ã€‘ 讨论

Canvas Backpack Leisure Travel,Backpack Outdoor Leisure,Leisure Backpack,Men Student School Bags

GDMK GROUP WEIHAI SHOES CO., LTD. , https://www.jinhoshoes.com